SpaceX did not just reopen the market for mega-IPOs.

It moved the center of the artificial intelligence trade from software and chips to orbit.

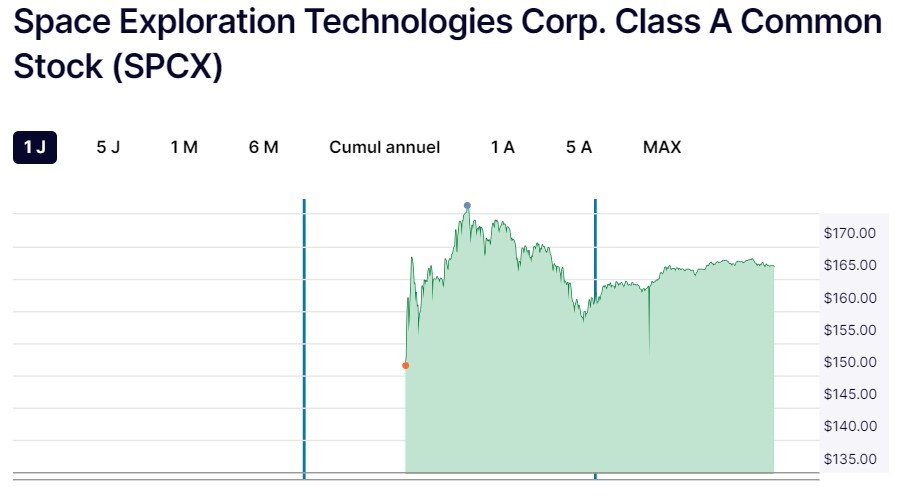

Elon Musk’s SpaceX raised $75 billion in the largest IPO on record, selling 555.56 million shares at $135 each and beginning trading on Nasdaq under the ticker SPCX. The stock opened at $150 and closed its first session at $160.95, giving the company a market value of roughly $2.1 trillion.

The listing more than tripled the previous IPO fundraising record held by Saudi Aramco, which raised $25.6 billion in 2019. It also turned SpaceX into one of the most valuable public companies in the US within a single trading day.

The bigger question is what investors actually bought.

This is no longer just the rocket company founded in 2002. The public SpaceX now sits at the intersection of launch services, satellite internet, AI infrastructure and Musk’s broader technology empire.

Investors are betting on a sprawling empire spanning rockets, satellites and AI, the public entity now includes Starlink, xAI and X.

That makes the IPO a live test of the market’s willingness to fund an unprofitable AI infrastructure story at trillion-dollar scale.

SpaceX generated about $18.7 billion in 2025 revenue, according to reports on its IPO disclosures. But the company also posted losses, with huge gap between its current earnings profile and its public-market valuation.

Investors are therefore paying for a future that has not yet been proven.

That future rests on three assumptions.

First, SpaceX can keep dominating launch economics. Second, Starlink can turn satellite broadband into a durable cash engine. Third, AI data centers in space can eventually become commercially viable.

The third assumption is the most speculative.

The idea of putting AI compute infrastructure in orbit speaks directly to the current bottlenecks in the AI economy: land, energy, cooling, latency, regulation and physical capacity. But it also adds a new layer of technical risk, including launch costs, maintenance, radiation exposure, replacement cycles and capital intensity.

That is why the IPO matters beyond SpaceX.

It is the first public-market stress test for the next phase of the AI boom.

The Market Is Buying Capacity Before Profits

For the past two years, public investors have mostly played AI through infrastructure proxies.

Nvidia became the clearest winner. Broadcom, AMD, Oracle, CoreWeave, Super Micro, Dell, Arista, Vertiv, Micron, SK Hynix and power companies also benefited from the view that AI demand would require more chips, memory, networking, cooling, power and data-center space.

That trade has been powerful.

Reuters reported that the MSCI AI index has gained 115% since early 2022, compared with a 44% rise in the broader MSCI World index. But the same report noted growing public anxiety over AI, with a Reuters/Ipsos poll finding that roughly three-quarters of Americans are concerned about the technology’s expanding use.

That disconnect is now central to the market.

Investors are pricing AI as the next industrial revolution. Many consumers and workers are still trying to understand whether it will help them or replace them.

SpaceX adds another layer to that debate.

Its valuation suggests investors are not only buying AI software. They are buying the possibility that the physical geography of AI infrastructure could change.

That is a bigger claim than ChatGPT adoption or enterprise automation.

It implies AI demand may become large enough to justify orbital infrastructure.

OpenAI and Anthropic Are the Next Test

The SpaceX listing comes just as OpenAI and Anthropic move closer to public markets.

OpenAI was founded in December 2015 by Sam Altman, Greg Brockman, Ilya Sutskever, Elon Musk, Wojciech Zaremba, and John Schulman. Anthropic was co-founded in 2021 by siblings Dario Amodei and Daniela Amodei, along with other former OpenAI executives.

Anthropic announced on June 1 that it confidentially submitted a draft S-1 registration statement to the US SEC for a proposed IPO. The company said the offering will depend on market conditions and other factors, and that the number of shares and price have not yet been finalized.

OpenAI followed with its own confidential S-1 submission. The company said it has not decided on timing and that “it may be a while,” because some steps may be easier to complete while it remains private.

That is likely to influence investor sentiment.

SpaceX gave the market a way to buy Musk’s space-and-AI infrastructure thesis. OpenAI and Anthropic would give investors direct exposure to the frontier model companies that have defined the generative AI boom.

But direct access could also change the trade.

If OpenAI and Anthropic list successfully, investors may rotate out of indirect AI plays and into the model companies themselves. That could reduce the scarcity premium that has supported chipmakers, cloud vendors and data-center stocks.

The result may not be a simple AI rally.

It could be a rotation inside AI.

What OpenAI and Anthropic IPOs Could Do to Stocks?

The first effect would be liquidity absorption.

Mega-IPOs do not occur in a vacuum. Large institutions need capital to buy them. That often means selling other holdings, especially crowded winners.

SpaceX already showed the scale of that problem.

Reuters reported that the IPO was approaching four times oversubscribed before pricing, while Bloomberg reported that retail orders alone topped $100 billion.

If OpenAI and Anthropic attempt similarly large listings, portfolio managers may have to decide which existing AI positions to trim.

The most vulnerable stocks would be companies that rallied mainly because investors lacked a direct way to own frontier AI labs.

The second effect would be valuation benchmarking.

If OpenAI or Anthropic trade well, private AI valuations may get another boost. That would help venture funds, late-stage investors and employees holding private shares.

If they trade poorly, the opposite could happen quickly.

Public markets would become the new judge of AI revenue quality, customer retention, compute cost and margin visibility. That would put pressure on late-stage AI startups whose private valuations depend on continued belief in exponential growth.

The third effect would be index concentration.

If SpaceX, OpenAI and Anthropic eventually join major benchmarks, passive funds could become more exposed to companies whose valuations depend heavily on future AI infrastructure profits.

That would tie retirement portfolios and index investors more closely to the AI cycle.

It would also raise the market’s sensitivity to AI disappointments.

The Profit Problem Is Getting Harder to Ignore

The biggest concern is not demand.

It is whether demand can be monetized at a level that pays for the infrastructure being built.

Oracle’s recent earnings reaction showed that investors are starting to ask that question more aggressively. Oracle spent about $55.66 billion in 2026, above its $50 billion target, as investors scrutinized its rising debt load and AI infrastructure spending.

That is the challenge across the AI stack.

Cloud companies must spend heavily before they know how profitable future AI workloads will be. Model companies must keep buying compute to stay competitive. Chipmakers must assume demand remains strong. Power providers and data-center developers must build capacity years ahead of confirmed cash flows.

This is why the SpaceX IPO is so important.

It suggests public investors are still willing to fund long-duration AI infrastructure stories.

But it does not prove those stories will generate returns.

Benjamin Lawrence, senior lead analyst at CB Insights, framed the valuation debate around that tension.

“SpaceX at 94x trailing revenue sounds insane, but annualizing its 2026 projections drops the forward multiple closer to 30x, albeit on optimistic run-rate estimates. Meanwhile, the LLM leaders face no moat and a retreat from ‘tokenmaxxing’ with a potential pullback in enterprise AI spend. Oddly enough, SpaceX may be the most reasonably priced, with OpenAI and Anthropic carrying the most risk,” Lawrence said.

The comment captures the market’s paradox.

SpaceX looks expensive on current numbers. Yet it owns physical infrastructure, launch capacity and Starlink distribution. OpenAI and Anthropic may have faster software revenue growth, but their long-term margins depend on model differentiation, pricing power and lower compute costs.

That may make the AI labs harder to value than SpaceX.

AI Funding Is Still Running at Record Speed

The private market has not slowed down.

CB Insights said global venture funding hit a record $286 billion in the first quarter of 2026, while exits fell to a two-year low. Its AI report said private AI companies raised more than $226 billion in Q1 2026, surpassing the full-year 2025 total in just three months.

Crunchbase reported that four of the five largest venture rounds ever recorded closed in Q1 2026, led by OpenAI, Anthropic, xAI and Waymo. The same report said those four companies collectively raised $188 billion, equal to 65% of global venture investment in the quarter.

The funding is spreading beyond chatbots.

xAI raised $20 billion in an upsized Series E round in January, with investors including Valor Equity Partners, StepStone, Fidelity, Qatar Investment Authority, MGX and Baron Capital. Reuters reported that Nvidia and Cisco Investments also participated, with the capital aimed partly at compute infrastructure

Waymo raised $16 billion at a reported $126 billion valuation, according to Crunchbase, showing that autonomous driving remains part of the broader AI capital cycle.

Jeff Bezos-backed Prometheus raised $12 billion in Series B funding round at a valuation of $41 billion. The industrial AI startup is focused on tools for designing and manufacturing complex physical products, including aerospace and medical devices.

Germany’s Neura Robotics raised $1.4 billion in a Series C round to scale its physical AI and robotics platform. The company said the round would help expand production and develop next-generation cognitive robots and humanoids.

The semiconductor side is also absorbing capital.

According to Semiconductor Engineering, chip-sector startups raised $8.4 billion in Q1 2026 across 80 companies. Crunchbase data showed semiconductor startups remained on pace for another large funding year.

This capital surge explains why AI markets feel both powerful and fragile.

The boom is broad enough to reshape public and private markets.

It is also concentrated enough that a failure by a few flagship companies could affect the entire chain.

What a Failure Would Mean?

The main risk is not that SpaceX, OpenAI or Anthropic disappear.

The risk is that they disappoint at the same time.

If SpaceX cannot turn Starlink, launch dominance and orbital AI infrastructure into durable profits, its valuation could become a problem for the entire space-tech sector.

If OpenAI and Anthropic fail to show a path to profitability, investors may start questioning the economics of frontier AI itself.

That would hit hardware first.

Nvidia, AMD, Broadcom, Marvell and TSMC are directly tied to AI compute demand. Any slowdown in model training, inference growth or custom-chip orders would affect expectations for the semiconductor cycle.

The next group would be cloud and infrastructure companies.

Microsoft, Amazon, Alphabet, Oracle and CoreWeave all depend on rising AI workloads to justify heavy capital spending. If AI labs slow spending or customers push back on prices, the cloud capex story could weaken.

Then come servers, networking and cooling.

Super Micro, Dell, Hewlett Packard Enterprise, Arista, Cisco and Vertiv have all benefited from AI data-center demand. These businesses are more exposed to order timing and inventory cycles.

Power companies would also feel it.

Vistra, Constellation Energy, Eaton, Schneider Electric and Quanta Services have been pulled into the AI infrastructure trade because data centers require massive power supply, grid upgrades and electrical equipment.

The private-credit market could be next.

Apollo and Blackstone are financing part of a $35 billion AI computing-capacity expansion tied to Anthropic and Broadcom. Apollo said a broader Broadcom-Apollo-Blackstone platform is designed to accelerate more than 20 gigawatts of global AI deployments.

That makes AI no longer just an equity story.

It is becoming a credit story, an energy story and a construction story.

If utilization disappoints, lenders may reassess risk across data-center financing. That would affect private credit, infrastructure funds and real-estate investors.

Venture Capital Would Face a Valuation Reset

Venture capital would be exposed in a different way.

AI valuations have become a major source of paper gains for late-stage funds. Strong public listings would validate those marks. Weak listings would force markdowns.

That would directly impact Sequoia, Andreessen Horowitz, Founders Fund, Thrive, SoftBank and other large backers of the AI cycle.

It would also impact limited partners.

Pension funds, endowments, sovereign wealth funds and family offices have exposure to private AI through venture funds, growth funds and crossover vehicles.

If AI IPOs fail, the damage would not stay inside Silicon Valley.

It would affect fundraising, secondary sales, employee liquidity and the willingness of investors to back the next generation of AI startups.

The exit market is already under pressure.

CB Insights said global exits fell to a two-year low in Q1 2026, even as funding hit a record. That imbalance means more capital is entering private companies while fewer liquidity events are returning cash to investors.

Mega-IPOs are supposed to solve that problem. But they could also expose it.

The Big Question. What about Bitcoin?

Bitcoin is watching the AI IPO wave from the sidelines.

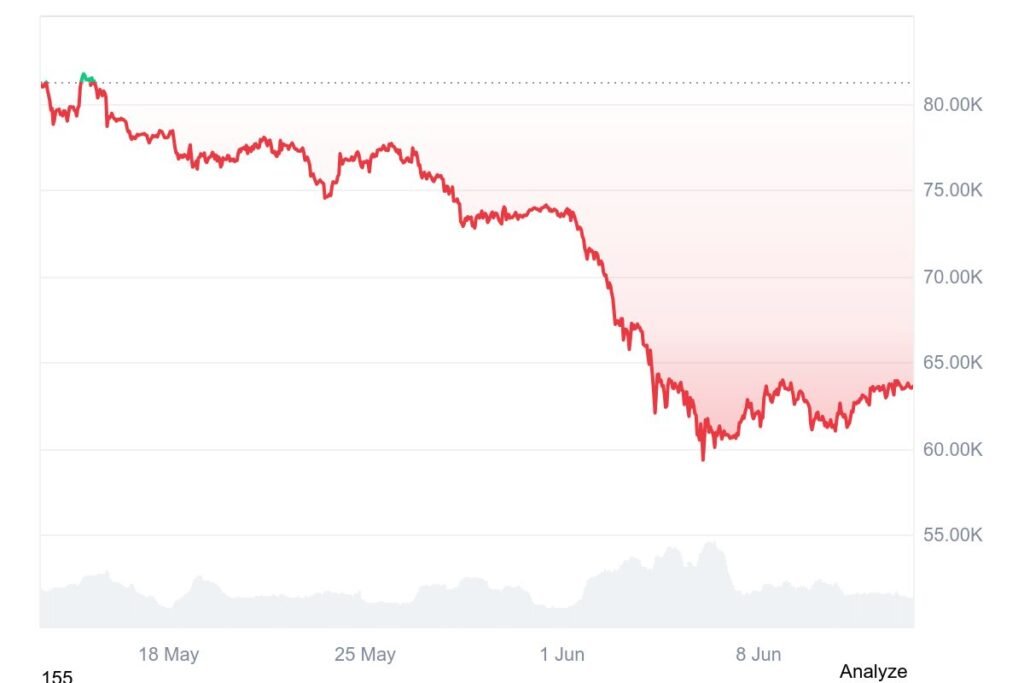

Bitcoin traded near $63,587 on June 13, with an intraday range between $62,855 and $64,305, according to CoinMarketCap market data. Bitcoin has declined over 20% in the last 1 month.

MarketWise founder Porter Stansberry recently argued that Bitcoin is trading far below his estimate of fair value because risk capital has moved into AI and semiconductor stocks. Stansberry’s model put Bitcoin’s fair value at $134,000, and he attributed the gap partly to capital rotating into Nvidia and other memory stocks.

That argument now faces a short-term test.

If OpenAI and Anthropic listings attract massive demand, speculative capital may remain tied up in AI. That could keep Bitcoin under pressure, especially if traders prefer new AI equity exposure over crypto risk.

In that scenario, the short-term impact on Bitcoin would likely be negative.

Crypto would be competing with the most anticipated equity listings in years.

But there is a second scenario.

If SpaceX becomes volatile, or if OpenAI and Anthropic struggle to justify their valuations, capital may rotate away from AI. Bitcoin could then benefit from the perception that AI equities are overextended while crypto has already repriced.

That would support Stansberry’s thesis. However, the first reaction to a failed AI IPO may still be risk-off selling.

Bitcoin often behaves like a high-beta asset during liquidity shocks. If markets sell AI, semiconductors and growth stocks together, crypto may fall first before any longer-term rotation into hard-asset narratives develops.

That is the key distinction.

Bitcoin may benefit from an AI valuation reset over time.

But in the immediate aftermath of a market shock, it may not behave like a safe haven.

Crypto Miners Are the Crossover Trade

Bitcoin miners sit at the intersection of both markets.

Some mining companies have repositioned themselves as AI infrastructure providers because they already control power access, land and data-center expertise.

That gives them a potential upside if AI infrastructure demand remains strong.

It also exposes them to a new risk.

If AI data-center economics weaken, the premium attached to mining companies with AI ambitions could disappear quickly.

Reuters has already warned that SpaceX’s blockbuster IPO may pull capital away from crypto in the short term, while MarketWise has argued that some Bitcoin mining stocks have outperformed Bitcoin because investors increasingly view them as AI data-center plays.

That makes miners a useful signal.

If miners keep rising while Bitcoin stalls, the market is still rewarding AI infrastructure over crypto monetary exposure.

If miners fall with AI stocks while Bitcoin stabilizes, the rotation may be changing.

The Global Economy Is Now Tied to the AI Capex Cycle

The AI boom is no longer confined to venture funding and software valuations.

It is shaping power demand, construction, chip manufacturing, cloud spending, debt issuance and public-market concentration.

That makes the downside larger.

A slowdown would hit suppliers, landlords, utilities, lenders, employees and local governments that planned around AI-driven investment.

It would also affect national industrial policy.

The US, Europe, China, Japan, South Korea and Gulf states are all trying to secure AI infrastructure, chip capacity and compute access. A broad AI reset would force governments to reassess subsidies, energy plans and strategic technology spending.

The comparison with previous bubbles is imperfect.

Unlike many dot-com-era companies, today’s AI leaders have real revenue, real users and real infrastructure demand.

But the valuation question is similar.

Can the eventual profits justify the capital now being spent?

That is still unanswered.

What to Watch Next?

The first thing to watch is SpaceX’s second week of trading.

A 19% first-day gain shows demand. It does not prove durable ownership. The key signals will be volatility, institutional buying, retail flows and whether the stock holds above its IPO price after the opening momentum fades.

The second is SpaceX’s post-IPO disclosure cycle.

Investors will need clearer evidence on Starlink margins, launch economics, xAI losses, capex intensity and the timeline for any orbital data-center business.

The third is OpenAI’s public S-1.

The confidential filing gives OpenAI optionality, but the public version will be more important. Investors will focus on revenue, losses, compute commitments, customer concentration, Microsoft economics and risk disclosures.

The fourth is Anthropic’s filing.

Anthropic has not set IPO terms yet. Its public disclosure will show whether the company has a cleaner enterprise AI model, better margins or lower compute intensity than rivals.

The fifth is AI capex guidance from hyperscalers.

Microsoft, Amazon, Alphabet, Meta and Oracle will show whether AI infrastructure spending is still accelerating or entering a more selective phase.

The sixth is Bitcoin’s response.

If Bitcoin fails to rally while AI IPOs absorb capital, the market may be confirming that risk appetite remains concentrated in AI. If Bitcoin rises during AI volatility, the rotation may be starting.

The seventh is the credit market.

AI is increasingly funded through large infrastructure platforms, private credit and debt issuance. Any widening in spreads or reduced appetite for AI-linked financing would be an early warning signal.

SpaceX proved investors are still willing to pay extraordinary prices for extraordinary promises.

OpenAI and Anthropic will test whether that appetite extends to the model companies at the center of the AI boom.

The market has funded the future. Now it will ask whether the future can produce cash flow.

More From BlockFirms

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Read our Editorial Policy. Parts of this article were drafted/ researched with the assistance of AI tools and subsequently reviewed, edited, and verified by the author and our editorial team to ensure accuracy and journalistic integrity. The final version reflects human editorial judgment and fact-checking. Read our AI Policy.